For Immediate Release

Contact: James Van Dyke, Javelin Strategy and Research

jvd@javelinstrategy.com

925-462-6599

Contact: Holly Cherico, Council of Better Business Bureaus, Inc.

hcherico@cbbb.bbb.org

703-247-9311

SAN FRANCISCO, January 31, 2006

- The 2006 Identity Fraud Survey Report - released by the Council of

Better Business Bureaus and Javelin Strategy & Research - provides

new facts on how identity fraud occurs, counterintuitive insights that

challenge conventionally accepted beliefs about these crimes, and steps

consumers can take to further protect themselves against this problem. Identity fraud is defined as access to personal account information that leads to fraud.

The comprehensive, longitudinal survey, independently produced

by Javelin Strategy & Research, is believed to be the largest ever

on identity fraud, with an increased 2005 sample size of 5,000

telephone interviews with consumers. The survey was, in part, made

possible by CheckFree, Visa and Wells Fargo & Company. The findings

show that despite growing fears the growth of identity fraud is

contained and that data compromise through the Internet is actually

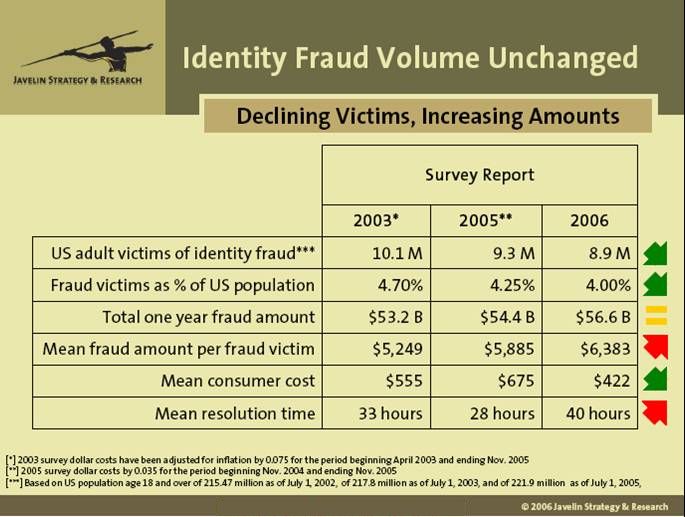

less severe, less costly and not as widespread as previously thought. Identity fraud victims as a percent of the United States adult

population have declined slightly from 4.7% to 4.0%, between 2003 and

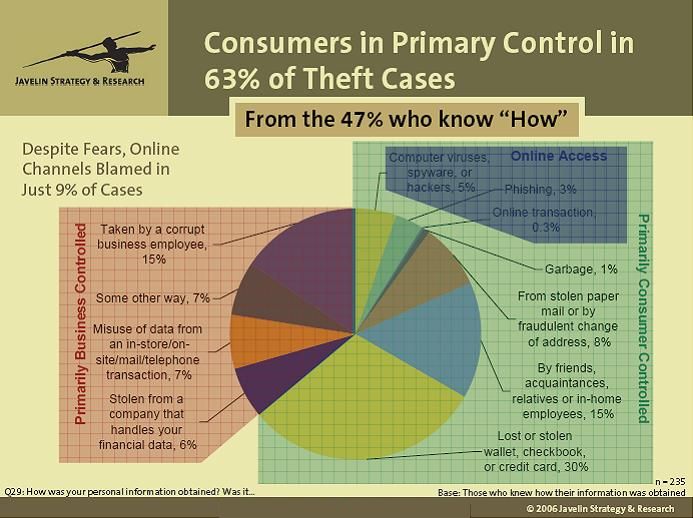

2006. Consumers need to be aware of the 63% of potential identity fraud

that is under their primary control. "Our numbers clarify four key misperceptions about identity

fraud," says James Van Dyke, Javelin's founder and principal analyst,

who oversaw the Identity Fraud Survey Report for the second consecutive

year. "Most importantly, people are not helpless in protecting

themselves from identity theft. Contrary to popular belief, consumers

do not bear the brunt of financial losses from identity fraud, Internet

use does not increase the risk of identity fraud; and that seniors are

not the most frequent targets of fraud operators. Our findings will

help people learn about specific important steps they can take to

better protect themselves.

10 Key Data Points on Identity Fraud

The 2006 Identity Fraud Report offers 10 key data points on identity fraud:

Identity fraud trends

- The number of adult victims of identity fraud within the

past 12 months has declined marginally between 2003 and 2006, from 10.1

million people to 8.9 million people, in the United States.

- The average fraud amount per case has increased from

$5,249 to $6,383, over 2 years. As a result, the total one-year cost of

identity fraud in the United States has remained relatively flat

between 2003 and 2006, increasing from $53.2 billion to $56.6 billion.

- The vast majority of identity fraud victims (68%)

incur no out-of-pocket expenses. This points out that businesses are

victims of fraud as well.

- Victims are spending more time to resolve identity fraud cases, which has increased from 33 hours in 2003 to 40 hours in 2006.

Means of Access

- Most data compromise - 90 percent - takes place

through traditional offline channels and not via the Internet, when the

victim can identify the source of data compromise.*

- Lost or stolen wallets, checkbooks or credit cards

continue to be the primary source of personal information theft when

the victim can identify the source of data compromise. (30 percent).*

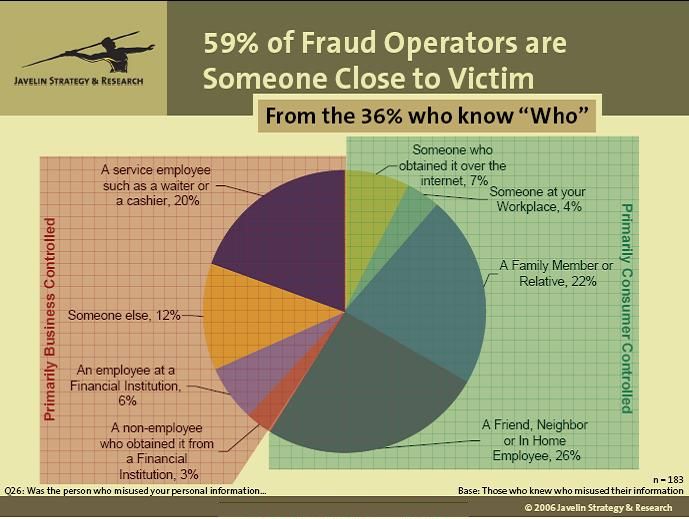

- Almost half (47 percent) of all identity theft is

perpetrated by friends, neighbors, in-home employees, family members or

relatives - someone known - when the victim can identify the

perpetrator of data compromise.**

- Nearly 70 percent of consumers are shredding documents, so that trash as a source of data compromise is now less than 1 percent.

Note: * 47% of victims could identify the source of the data compromise.

** 36% of victims could identify the person who misused their information.

Demographic differences:

- The 65+ demographic age group has the smallest rate of identity fraud victims (2.3%).

- The 35-44 demographic age group has the highest average

fraud amount ($9,435). (Note: victims' age was not found to be

statistically related to Internet usage as compared to traditional

types of fraud.)

Clarifying Four Key Misperceptions Surrounding Identity Fraud

- Misperception #1: "Consumers are helpless to protect themselves"

- In 63% of fraud cases, the point of compromise was either

theft by close associates of the consumer (friends, family, neighbors,

etc.), lost or stolen wallets, cards and checkbooks, breached home

computers or stolen mail or trash.

- Consumers detect almost half (47%) of identity fraud

cases. Self-detection is faster (averages 67 days vs. 101 days),

results in smaller average fraud amounts ($4,431 vs. $8,466) and

smaller consumer costs ($347 vs. $538).

- A key way to detect fraudulent accounts is through

credit monitoring / reports. Eleven percent of fraud cases were caught

via this means.

- Misperception #2: "Consumers bear the brunt of the financial losses from identity fraud"

- Average out-of-pocket cost for identity fraud victims is

$422 (7% of the average fraud amount of $6,383) down from $675 last

year and $555 in 2003.

- Misperception #3: "Internet use increases the risks of identity fraud"

- Data compromise through the Internet is statistically unchanged from last year (11% to 9% today).

- Internet use can lead to lower damages from identity

fraud. Electronic account monitoring is the fastest way to detect fraud

and leads to lower losses - (22 days and $3,806).

- Misperception #4: " Seniors are most frequent targets of fraud operators"

- Generation X (ages 25-34) has the highest rate of identity

fraud at 5.4 percent. The average fraud amount for this demographic is

$6,270 as compared to the average fraud amount for the 65+ segment

which is $2,665.

Identity Safety Tips That Can Protect Consumers

"This new research offers a very different but accurate and

helpful perspective about identity theft fraud and it shows how we can

stay on top of this problem," says Steven J. Cole, president and CEO of

the Council of Better Business Bureaus. "Consumers can do a lot to make

sure they cut down the risk associated with this fraudulent activity." Based on the latest findings, the Better Business Bureau,

Wells Fargo, Visa and CheckFree have issued the following tips for

consumers to protect themselves against financial identity fraud:

PREVENT access to your personal information

- Do not release Social Security or account numbers in

response to e-mail, phone or in-person requests. When responding to

e-mail, ignore any Internet links provided and type the full address

instead.

- Keep all sensitive documents, checkbooks and credit cards securely locked away at home and at work.

- Carry only those credit cards that you need in your wallet.

- Before discarding, shred all private documents.

- Retrieve paper mail promptly and place outgoing checks or other sensitive documents in a U.S. Postal Service mailbox.

- Sign up for automatic payroll deposits.

- Replace paper bills, statements and checks with online (paperless) versions.

- Keep passwords hidden (even in your own home) and change them frequently.

- Use and regularly update firewall and anti-virus software.

- Do not respond to suspicious e-mails. Delete them, and

if there is any doubt contact the company to determine if the e-mail is

real.

- Don't discard a computer without completely destroying the data on the hard drive.

DETECT unauthorized activity

- Review bank, credit card and biller statements weekly - available through online account access.

- Contact your financial provider if you fail to receive statements in a timely manner.

- Review your credit information regularly (free annual reports are available at www.annualcreditreport.com or call 1-877-322-8228).

- Use e-mail-based account "alerts" to monitor transfers,

payments, low balances, withdrawals, or detect any out-of-pattern

activity.

- Visit your bank's, credit card issuer's or biller's web site(s) frequently to monitor regular account activity.

RESOLVE fraud promptly, minimizing losses and protecting your credit record

- Ask your financial provider about zero-liability guarantees

against fraud and dedicated resources to help you resolve and recover

from any potential losses.

- Victims of theft: notify your financial providers,

begin monitoring your accounts more frequently, and place an "alert" at

all three credit bureaus (Equifax, Experian or TransUnion).

- Alert federal and local law enforcement if you suspect or detect identity fraud.

For more information on the methodology used for this study and visuals of key findings, visit www.idsafety.net.

How Safe Are You? Take an Identity Safety Quiz

The Better Business Bureau has co-released an Identity Safety

Quiz so consumers can determine if their typical behavior places them

at greater risk of becoming an identity fraud victim and what specific

steps they can take to reduce that risk and increase their safety. The

quiz can be accessed at www.idsafety.net.

For additional educational tips, please access:

www.bbb.org/idtheft; www.checkfree.com/idprotect; www.consumer.gov/idtheft/; www.visa.com/security; www.wellsfargo.com/privacy_security/fraud_prevention/.

About the Better Business Bureau

The Better Business Bureau (BBB) system (www.bbb.org)

is is dedicated to fostering fair and honest relationships between

businesses and consumers, instilling consumer confidence and

contributing to an ethical business environment, in both the

traditional and online marketplaces. The first BBB was founded in 1912,

and the network of BBBs and the Council of Better Business Bureaus have

grown to become the most recognized advocate for promoting ethical

business and advertising practices, providing more than 60 million

instances of service to consumers and businesses in 2004. BBBs in the

U.S. and Canada are supported by 375,000 business members throughout

North America. About Javelin Strategy and Research

Javelin provides research-based strategic direction for financial

services, payments, e-commerce, and identity fraud. Javelin rigorously

researches technology issues, industry trends, attitudes and activities

of consumers, small businesses, institutions, processors, merchants,

billers, and other organizations in order to deliver relevant,

high-impact strategic guidance. Javelin can be found on the Web at www.javelinstrategy.com.

For more information on this project or other Javelin studies, visit www.idsafety.net or www.javelinstrategy.com/reports/

Addendum: Key Findings

|